Dividend Investing: Build a Recession-Resilient Income Portfolio

Updated: May 2026 | By Jenna Lofton, StockHitter.com

Jenna’s Bottom Line

Dividend investing is not about finding the highest yield. It is about finding businesses that generate enough cash to pay you consistently, grow that payment over time, and still have enough left over to fund their own growth. Those businesses exist. Finding them requires more than sorting a stock screener by yield and picking the top five.

Key Takeaways

- Dividend investing builds income from stocks that pay regular cash distributions. The income arrives regardless of what the stock price does on any given day.

- The payout ratio, free cash flow coverage, and consecutive years of dividend growth matter more than the yield itself. A 7 percent yield from an unsustainable business is a trap. A 3 percent yield from a business compounding that payment at 10 percent annually is a compounding machine.

- Dividend growth investing and high yield investing are two distinct strategies with different risk profiles. Knowing which one you are doing matters.

- The dividend yield trap is one of the most common mistakes in income investing. A rising yield caused by a falling stock price is often a warning signal, not a buying opportunity.

- In 2026, with approximately $9.2 trillion still sitting in cash globally, dividend stocks offer one of the most compelling ways to generate income while remaining invested in equities.

Why Dividend Investing Works

The case for dividend investing comes down to one thing most investors underestimate: income that arrives regardless of what markets do.

When a stock price falls 20 percent in a bear market, a growth investor’s only return is on paper and it is negative. A dividend investor with the same position is still collecting quarterly payments. That income provides a psychological anchor that makes holding through volatility dramatically easier, which means fewer panic sells at the worst possible moments.

The compounding effect of reinvesting those dividends over time is where the real wealth building happens. Dividends reinvested buy more shares. Those shares generate more dividends. The cycle compounds quietly in the background while the financial media obsesses over daily price movements.

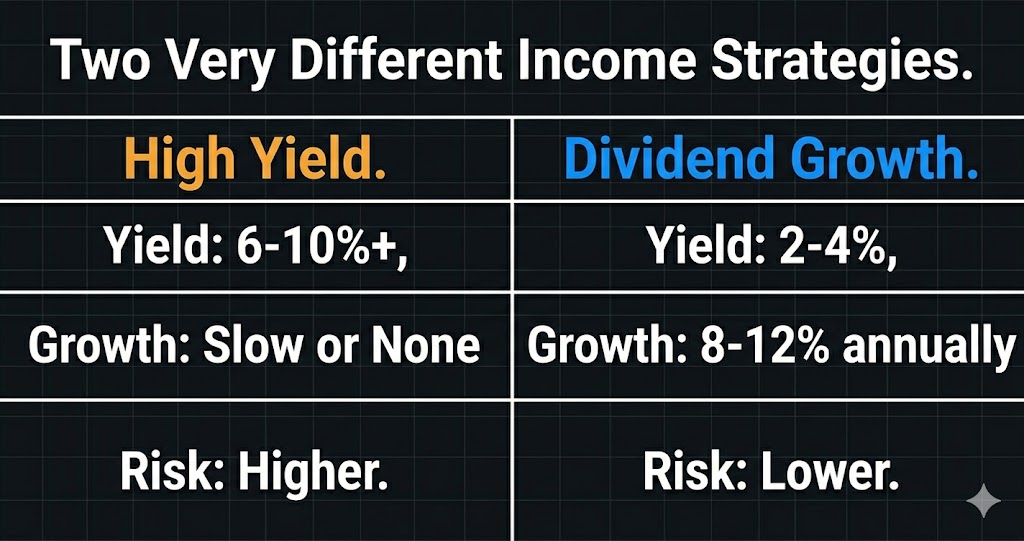

The Two Types of Dividend Stocks

Before buying anything, I want to know which type of dividend stock I am dealing with. They require completely different analysis and suit completely different investor situations.

High yield dividend stocks pay large current income, often 6 to 10 percent or more. The yield is attractive on paper. The risk is that high yields frequently signal a business under stress, where the market has driven the stock price down precisely because investors doubt the dividend’s sustainability. Chasing yield without understanding why it is high is one of the fastest ways to lose money in income investing.

Dividend growth stocks pay lower current yields, typically 2 to 4 percent, but grow that payment consistently year after year. A stock yielding 3 percent today that grows its dividend at 10 percent annually doubles the income per share in roughly seven years. Over a 20-year holding period, the yield on original cost can reach double digits while the stock price has appreciated significantly. This is the approach I favor for long-term wealth building.

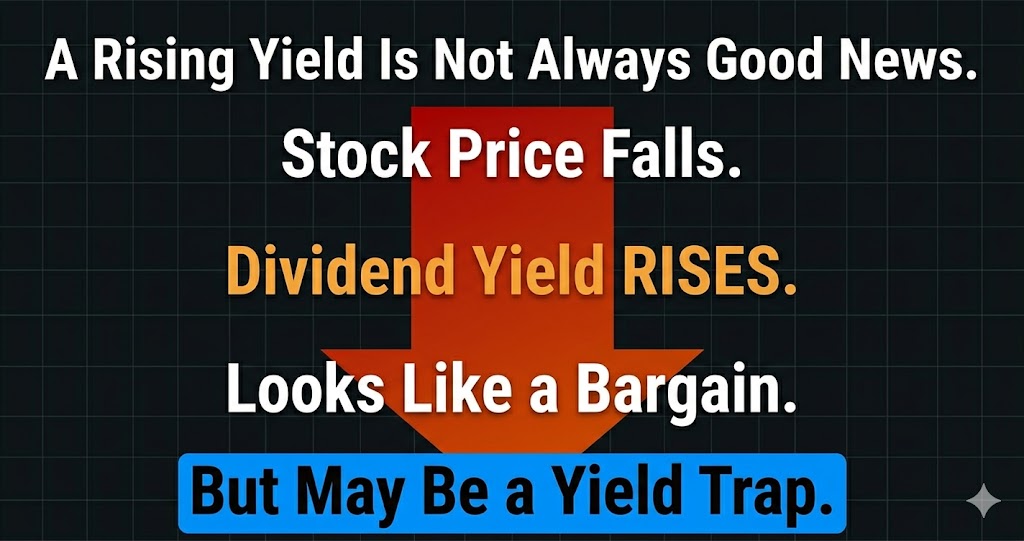

The Dividend Yield Trap Explained

This is the mistake I see most often from investors new to income investing and it is completely avoidable once you understand the mechanics.

Dividend yield is calculated by dividing the annual dividend payment by the current stock price. When a stock price falls, the yield rises mathematically even if the dividend has not changed. A stock paying $4 annually that trades at $100 yields 4 percent. If the stock falls to $50, the yield appears to double to 8 percent. That looks attractive. It is often a trap.

The stock price fell for a reason. If that reason is deteriorating business fundamentals, the dividend is likely to be cut next. Investors who buy the apparent bargain collect one or two payments before the cut, then watch the stock fall further when the cut is announced. They end up with a lower yield, a capital loss, and the frustration of having done exactly what the yield number seemed to suggest they should.

The test I run before buying any high-yield stock is simple. Ask why the price fell. If the answer is temporary market pessimism about a business with durable cash flow, the yield may be genuinely attractive. If the answer involves declining revenue, rising debt, or industry disruption, move on.

The Metrics That Actually Matter

Yield gets all the attention. These are the numbers I actually care about:

- Payout ratio. The percentage of earnings paid out as dividends. A payout ratio below 60 percent means the business retains enough earnings to fund growth while sustaining the dividend. Above 80 percent and the dividend has limited room to grow and is vulnerable to any earnings disappointment. Above 100 percent means the business is paying out more than it earns, which is unsustainable.

- Free cash flow coverage. Earnings can be manipulated by accounting choices. Free cash flow is harder to fake. I want to see free cash flow comfortably covering the dividend payment, ideally at 1.5 times or more. A dividend funded by free cash flow is durable. A dividend funded by borrowing is not.

- Consecutive years of dividend growth. A company that has grown its dividend for 10 or more consecutive years has maintained that commitment through at least one or two economic downturns. That track record is a meaningful signal of management’s commitment and the business’s cash generation consistency. The S&P 500 Dividend Aristocrats are companies that have grown dividends for at least 25 consecutive years. That list is a useful starting point for quality screening.

- Debt level. Highly leveraged companies face competing demands on cash flow between debt service and dividend payments. When business conditions deteriorate, debt gets paid first. Companies with low or manageable debt have the flexibility to maintain dividends through economic cycles that heavily indebted competitors cannot.

Dividend Investing in Recessions

This is where dividend investing earns its keep most visibly. Bear markets and recessions are brutal for growth investors. For a well-constructed dividend portfolio, they are uncomfortable but manageable.

Defensive sectors that produce reliable dividend income tend to hold value better during economic contractions. Consumer staples companies like Procter and Gamble and Coca-Cola sell products people buy regardless of economic conditions. Utilities generate regulated, predictable revenue. Healthcare demand does not disappear in recessions. These businesses cut dividends far less frequently than cyclical businesses, which is exactly what you want when markets are falling.

The income from dividends during a bear market also provides a psychological and financial anchor. Collecting 3 to 4 percent annually in dividends while the stock price is down 15 percent is a very different experience from holding a growth stock down 40 percent generating no income whatsoever. The dividend does not make the loss disappear. It makes staying invested through the recovery significantly easier.

For our full guide on positioning a dividend portfolio specifically for recessionary periods, see our guide to how to invest in a recession.

Experience Transparency

My early dividend investing experience was almost entirely yield chasing and I paid for it. I bought a handful of high-yield energy partnerships in 2015 yielding 8 to 10 percent that looked like income machines. When oil prices collapsed, the distributions got slashed, the unit prices fell 40 to 60 percent, and I ended up with realized losses that took years to recover. The lesson was not that high yield is always bad. It is that yield without understanding what generates it is speculation dressed up as income investing. I rebuilt my dividend approach entirely around free cash flow coverage and consecutive growth history after that. I have not held a position yielding above 6 percent since unless the free cash flow math was airtight.

Dividend Investing and AI Infrastructure

Most people do not think of AI infrastructure and dividend investing in the same sentence. Broadcom (AVGO) is the reason they should.

Broadcom has grown its dividend at a compound annual rate of over 20 percent for more than a decade while also being one of the primary beneficiaries of AI chip and networking infrastructure demand. The current yield is modest by income investing standards, but the growth rate of that payment and the free cash flow generation supporting it make it one of the highest quality dividend growth positions available in the technology sector.

This is what I mean when I say dividend investing does not have to mean abandoning growth. The best dividend growth businesses are often also the best businesses, full stop. They generate enough cash to reward shareholders, fund their own expansion, and still have capacity left over. For our full breakdown of Broadcom as both a growth and income position, see our individual analysis at Broadcom stock.

The Dividend Investing Checklist

Before I add any dividend position to a portfolio I run through these five questions. If a stock fails more than one of them I do not buy it regardless of how attractive the yield looks.

- Is the payout ratio below 60 percent? Room to grow and room to absorb an earnings miss without cutting.

- Has the dividend grown for at least five consecutive years? Ideally ten or more. This filters out businesses that started paying dividends recently and have not been tested through a downturn.

- Does free cash flow cover the dividend by at least 1.5 times? The business generates real cash, not just accounting earnings.

- Is the debt level manageable? Debt-to-EBITDA below 3 times is my general threshold. Higher than that and the dividend competes with debt service in a stress scenario.

- Is the revenue recession-resilient? If the business’s revenue collapses in an economic downturn, the dividend probably does too. I want businesses where people keep paying regardless of economic conditions.

Research Services Worth Using for Dividend Investing

Dividend investing looks simpler than growth or value investing on the surface. It is not. Identifying businesses with genuinely sustainable and growing dividends requires the same depth of financial analysis as any other approach, and the consequences of getting it wrong are particularly visible because the income you were counting on disappears.

The Oxford Income Letter from Marc Lichtenfeld is the research service I point dividend-focused investors toward most consistently. Lichtenfeld’s methodology focuses specifically on dividend sustainability, free cash flow coverage, and consecutive growth history rather than current yield, which is exactly the right framework. His approach to identifying what he calls “10-11-12” stocks, those with 10 percent or more dividend growth, 11 percent or more total return potential, and starting yields above 4 percent, is one of the more disciplined income investing frameworks I have seen at the retail level.

Wall Street Reality Check

The financial industry loves selling dividend products because income sounds safe and safe sounds like something you should pay for. ETFs, closed-end funds, and structured products built around income generation frequently charge fees that consume a significant portion of the very income they promise to deliver. A self-constructed dividend portfolio of 15 to 20 quality businesses costs nothing to hold beyond the initial research time. Before paying for income delivery, understand exactly what percentage of your dividend income is going to the vehicle delivering it. In most cases the answer is enough to matter over a decade of compounding.

Bottom Line

Dividend investing built around quality, free cash flow, and consistent growth history is one of the most reliable paths to long-term wealth available to individual investors. It requires ignoring the highest yields, doing the fundamental analysis behind the payment, and holding through the periods when the income feels boring compared to what growth stocks are doing. That boredom is frequently the strategy working exactly as intended.

Further Reading

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice. StockHitter.com and Jenna Lofton are not registered investment advisors. All investing involves risk, including the potential loss of principal. Past performance does not guarantee future results. Always conduct your own due diligence and consult a licensed financial professional before making investment decisions. Jenna Lofton holds a position in PLTR. Some links on this page may be affiliate links, meaning StockHitter.com may receive compensation if you subscribe to a service at no additional cost to you. This does not influence our editorial opinions.