How to Invest in a Recession in 2026

Updated: May 2026 | By Jenna Lofton, StockHitter.com

Jenna’s Bottom Line

Recessions feel like the worst time to invest. Historically, they are among the best. The investors who come out ahead are not the ones who predicted the recession. They are the ones who had a plan before it started and executed it while everyone else was panicking.

Key Takeaways

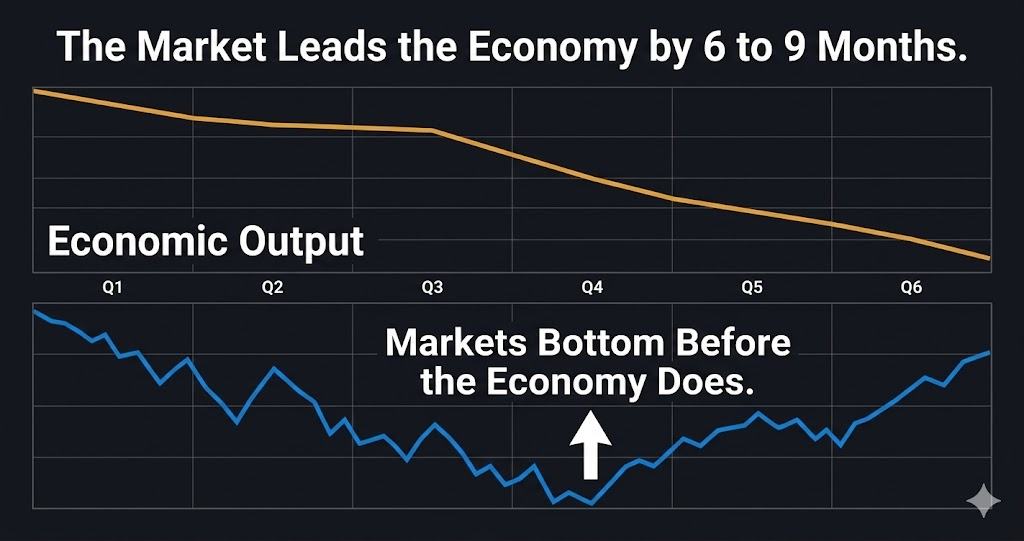

- The stock market typically bottoms 6 to 9 months before the economy does. Waiting for the recession to officially end before investing means missing most of the recovery.

- Defensive sectors including consumer staples, utilities, and healthcare historically outperform cyclical sectors during recessions.

- Dividend-paying stocks with strong balance sheets provide income and stability when growth stocks are getting repriced sharply lower.

- Eliminating margin debt before a recession is the single most important structural decision an investor can make.

- Recessions create the entry points for quality businesses at prices unavailable in normal markets. Cash reserves are what let you act on them.

What a Recession Is and What It Does to Markets

A recession is formally defined as two consecutive quarters of negative real GDP growth. The National Bureau of Economic Research (NBER) is the official arbiter of U.S. recession dates, using a broader set of indicators beyond just GDP.

Recessions cause corporate earnings to fall, unemployment to rise, and consumer spending to contract. Stock markets react to these deteriorating fundamentals by repricing equities lower, often sharply and well in advance of the economic data confirming the recession.

The critical insight for investors is that markets are forward-looking. The stock market typically bottoms 6 to 9 months before the economy does. By the time a recession is officially declared, much of the market decline is often already behind us.

Why Most Investors Get Recessions Wrong

The most common mistake investors make during recessions is waiting for certainty before acting. They want confirmation that the recession is ending before they buy. By the time that confirmation arrives in the economic data, the market has already recovered 20 to 30 percent.

The second most common mistake is panic selling near the bottom. Investors who hold through the early stages of a recession-driven decline often capitulate when the economic news is at its worst, which is typically very close to when the market is bottoming.

Both mistakes share the same root cause: using economic news as a buy signal instead of price and business value. Economic news tells you what already happened. Price tells you what the market currently expects. The two are almost never in sync at turning points.

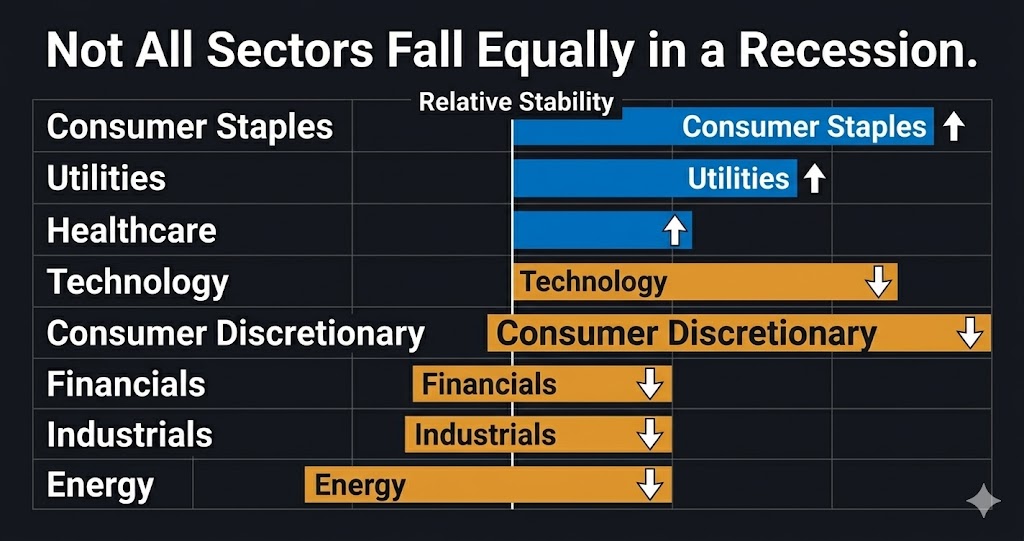

Sectors That Hold Up in Recessions

Not all sectors fall equally during recessions. Understanding which sectors are defensive and which are cyclical is one of the most practical tools for recession positioning.

Defensive sectors tend to outperform during recessions because their revenue is relatively insensitive to economic cycles:

- Consumer Staples. Companies selling food, beverages, household products, and personal care items. People buy toothpaste and groceries regardless of economic conditions. Procter and Gamble, Costco, and Walmart have historically held value better than the broad market during downturns.

- Utilities. Electric, gas, and water utilities generate stable, regulated revenue regardless of economic conditions. They also tend to pay consistent dividends that provide income when capital gains are scarce.

- Healthcare. Demand for medical services, pharmaceuticals, and healthcare equipment does not disappear in recessions. Johnson and Johnson, UnitedHealth Group, and large pharmaceutical companies have historically been relative safe havens.

Cyclical sectors tend to underperform because their revenue is directly tied to economic activity:

- Consumer Discretionary. Spending on restaurants, travel, luxury goods, and entertainment falls when consumers tighten budgets.

- Financials. Banks face rising loan defaults and compressed margins when the economy contracts.

- Industrials. Manufacturing and construction activity declines with business investment.

- Energy. Commodity prices typically fall with reduced economic activity, compressing margins for oil and gas producers.

The Case for Dividend Stocks in a Recession

Dividend-paying stocks serve two purposes during recessions that make them particularly valuable in a defensive portfolio.

First, dividends provide income regardless of what the stock price does. A company paying a 4 percent dividend yield continues paying that dividend even if the stock price falls 20 percent. That income provides a return floor that pure growth stocks cannot match during downturns.

Second, companies that maintain and grow dividends through recessions are signaling strong balance sheets and cash flow generation. A company that cannot sustain its dividend during an economic contraction cuts it, and dividend cuts are typically accompanied by sharp stock price declines. Companies with the financial strength to maintain dividends through recessions are the ones most likely to emerge in a strong competitive position.

For investors specifically looking to build a recession-resilient income portfolio, the Oxford Income Letter from Marc Lichtenfeld focuses on dividend investing with a particular emphasis on companies with the financial strength to maintain and grow dividends through economic cycles. It is one of the more rigorous dividend research services available, with a specific methodology for identifying sustainable dividend payers rather than yield traps.

What to Do With Bonds During a Recession

Treasury bonds historically rally during recessions as investors flee equities for safety and the Federal Reserve cuts interest rates to stimulate growth. When rates fall, bond prices rise, making existing bonds with higher yields more valuable.

The 10-year Treasury yield is one of the most watched indicators of recession expectations. A sharp drop in the 10-year yield typically signals that the bond market is pricing in slower growth and potential Fed rate cuts.

A portfolio with meaningful Treasury bond exposure going into a recession benefits from both the price appreciation of bonds and the stabilizing effect on overall portfolio volatility. The classic 60/40 portfolio, 60 percent equities and 40 percent bonds, was designed specifically to provide this kind of recession buffering.

The Role of Gold in Recession Investing

Gold is not a growth asset. It does not pay dividends or compound earnings. But it has historically served as a store of value during periods of economic stress, currency debasement, and financial system instability.

During the 2008 financial crisis, gold rose approximately 25 percent while the S&P 500 fell 57 percent. During the 2020 pandemic recession, gold reached all-time highs while equity markets crashed. The correlation between gold and equities during crisis periods is often negative, which makes gold a genuine diversifier rather than just a speculative asset.

For investors who want deeper analysis of gold as a recession hedge and macro asset, Jim Rickards’ Strategic Intelligence has a long-standing focus on gold, currency risk, and the systemic conditions that tend to drive precious metals higher. Rickards’ macro framework is particularly relevant during recessionary periods when traditional asset correlations break down.

What to Avoid in a Recession

Recession investing is as much about what to avoid as what to buy.

- Highly leveraged companies. Companies with high debt loads face rising interest costs and potential covenant violations when earnings fall. Their stocks often decline far more than the broad market and some do not survive recessions intact.

- Margin debt in your own portfolio. Leveraged investors face margin calls during market declines that force selling at the worst possible moment. Entering a recession with margin debt is one of the highest-risk positions an individual investor can hold.

- Speculative growth stocks with no earnings. Companies trading at extreme multiples on the expectation of future profits get repriced aggressively lower when the economic environment deteriorates and investor risk appetite collapses.

- Sector concentration in cyclicals. A portfolio heavily concentrated in consumer discretionary, financials, or industrials will significantly underperform a diversified portfolio during a recession.

Experience Transparency

The 2008 recession was the one that taught me the practical value of defensive positioning. I had minimal consumer staples and utilities exposure going into it because those sectors had underperformed the bull market and felt boring. They fell far less than the rest of my portfolio during the crash and paid dividends throughout. That experience permanently changed how I think about sector allocation. Boring sectors that pay you while you wait are not a concession to conservatism. They are a strategic asset when the cycle turns.

When to Start Buying During a Recession

The honest answer is that there is no reliable signal for the exact bottom. Investors who wait for certainty miss most of the recovery. Investors who try to catch the exact bottom almost never do.

The most practical approach is staged buying. Rather than deploying all available cash at once, committing a fixed percentage of cash reserves at regular intervals during a recession-driven decline captures some of the best prices without requiring perfect timing.

The historical data on what happens to investors who buy during recessions is consistent and compelling. Real GDP eventually recovers after every recession. Markets recover before it does. The investors who buy quality businesses at recession-depressed prices and hold through the recovery generate returns that normal market conditions rarely produce.

The Recession Investing Checklist

Before a recession arrives, or as early in one as possible, work through these five priorities in order:

- Eliminate margin debt. No leveraged position is worth the forced-selling risk during a market decline.

- Build a cash reserve. Three to six months of living expenses outside the investment portfolio, plus additional dry powder for buying opportunities.

- Shift toward dividend payers. Rotate toward companies with strong balance sheets, consistent dividend histories, and recession-resilient revenue streams.

- Reduce cyclical exposure. Trim positions in highly cyclical sectors before they get repriced aggressively lower.

- Identify your buy list. Make a list of quality businesses you want to own more of at lower prices. Having that list ready before the decline means you can act on it rather than freeze.

For the broader context on how recessions fit into the larger pattern of market cycles, see our pillar guide to market cycles explained. For a deeper look at what specifically triggers recessions and market crashes, see our guide to what causes stock market crashes.

Wall Street Reality Check

Wall Street firms spend enormous resources on recession prediction models. Most of them fail to predict recessions with enough lead time to be actionable, and many generate false positives that cause investors to de-risk prematurely and miss bull market gains. The more useful question is not when the next recession will start but whether your portfolio is structured to survive one whenever it arrives. A portfolio built for recession resilience does not require recession prediction. It just requires discipline applied before the pressure is on.

Bottom Line

Recessions are temporary. The market bottoms before they end. The investors who come out ahead are the ones who eliminated leverage, built cash reserves, shifted toward defensive positioning, and had a buy list ready before the decline started. You do not need to predict recessions to survive them. You need a plan that works regardless of when they arrive.

Further Reading

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice. StockHitter.com and Jenna Lofton are not registered investment advisors. All investing involves risk, including the potential loss of principal. Past performance does not guarantee future results. Always conduct your own due diligence and consult a licensed financial professional before making investment decisions. Jenna Lofton holds a position in PLTR. Some links on this page may be affiliate links, meaning StockHitter.com may receive compensation if you subscribe to a service at no additional cost to you. This does not influence our editorial opinions.