Bull Market vs. Bear Market: What It Means

Updated: May 2026 | By Jenna Lofton, StockHitter.com

Jenna’s Bottom Line

Bull markets reward patience. Bear markets reward preparation. The investors who build serious wealth over time are not the ones who predicted which was coming. They are the ones who had a plan for both before either arrived.

Key Takeaways

- A bull market is a rise of 20 percent or more from a recent low. A bear market is a decline of 20 percent or more from a recent high.

- The average bull market lasts approximately 6.6 years and gains roughly 339 percent. The average bear market lasts about 1.3 years and loses roughly 38 percent.

- Bull markets move through three emotional stages: skepticism, confidence, and euphoria. Knowing which stage you are in helps you calibrate risk.

- Bear markets end when pessimism reaches maximum. The investors who buy at that point generate the best long-term returns.

- The single most expensive mistake investors make is selling during a bear market and waiting too long to re-enter. The math on missing the recovery is brutal.

What a Bull Market Is

A bull market is formally defined as a sustained rise of 20 percent or more from a recent low. The term originated from the way a bull attacks, thrusting its horns upward. It has been applied to rising markets for over a century.

In practice, bull markets feel less like a single event and more like a long, uneven climb interrupted by corrections that feel alarming but resolve upward. Most investors do not realize they are in a bull market until it has been running for a year or more.

Bull markets are the historical default condition of equity markets. The S&P 500 has spent far more time in bull markets than bear markets over any meaningful time horizon. Understanding this is the foundation of long-term investing conviction.

What a Bear Market Is

A bear market is a decline of 20 percent or more from a recent high, sustained over at least two months. The term comes from the way a bear attacks, swiping its paws downward.

The two-month requirement matters. A sharp crash that recovers quickly, like the 34 percent S&P 500 decline in February and March 2020 that recovered within months, technically meets the price threshold but behaves very differently from a grinding multi-year decline like 2007 to 2009.

Bear markets are painful, inevitable, and temporary. Every single bear market in S&P 500 history has ended in a recovery that exceeded the prior peak. That fact is easy to state and genuinely difficult to hold onto when you are 18 months into a decline with no bottom in sight.

How Bull Markets Actually Feel

Bull markets move through three distinct emotional stages. Most investors only recognize which stage they were in after the fact.

The early bull market is defined by skepticism. Prices are rising off a recent low but the prevailing sentiment is disbelief. Most investors are still too scarred by the prior bear market to trust the rally. This is where the best entry points exist and where the fewest investors are willing to act.

The mid bull market is defined by growing confidence. Economic data is improving, corporate earnings are rising, and the financial media has shifted from cautious to constructive. More investors are participating. Valuations are reasonable. This is the phase that feels most comfortable and produces the steadiest compounding.

The late bull market is defined by euphoria. Valuations are stretched. Every dip gets bought aggressively. New investors who sat out the early and mid phases are entering the market in large numbers, convinced they are not too late. This is where risk is highest, even though it feels lowest.

How Bear Markets Actually Feel

Bear markets also move through recognizable emotional stages. Understanding them does not make bear markets painless. It makes them navigable.

The early bear market is characterized by denial. Prices are falling but most investors assume it is a correction that will resolve quickly. This phase is where the most dangerous inaction occurs, because investors who should be reducing risk tell themselves to wait for a recovery that is not coming.

The mid bear market is characterized by fear. The decline has been large enough that it can no longer be dismissed as a correction. Corporate earnings are disappointing. Economic data is deteriorating. Media coverage is relentlessly negative. Selling accelerates as investors who held through the early phase capitulate.

The late bear market is characterized by capitulation. This is the point of maximum pessimism. Investors who have held through the entire decline finally sell, often at the worst possible moment. Volume spikes. Volatility peaks. And then, usually with no obvious positive catalyst, the market begins to recover.

Experience Transparency

The hardest part of investing through bear markets is not the math. It is the social environment. In 2009, virtually everyone I knew in finance had a compelling argument for why the recovery would take a decade. The data supported their pessimism. The structural argument was sophisticated. They were wrong. The investors who bought S&P 500 index funds in March 2009 and held for five years made roughly 200 percent. The ones who waited for certainty before re-entering missed most of it. Bear markets feel permanent when you are inside them. They never are.

The Historical Record

The long-term historical record of bull and bear markets is one of the most useful datasets in investing. It provides the context that prevents panic during downturns and overconfidence during rallies.

Key historical data points from S&P 500 history:

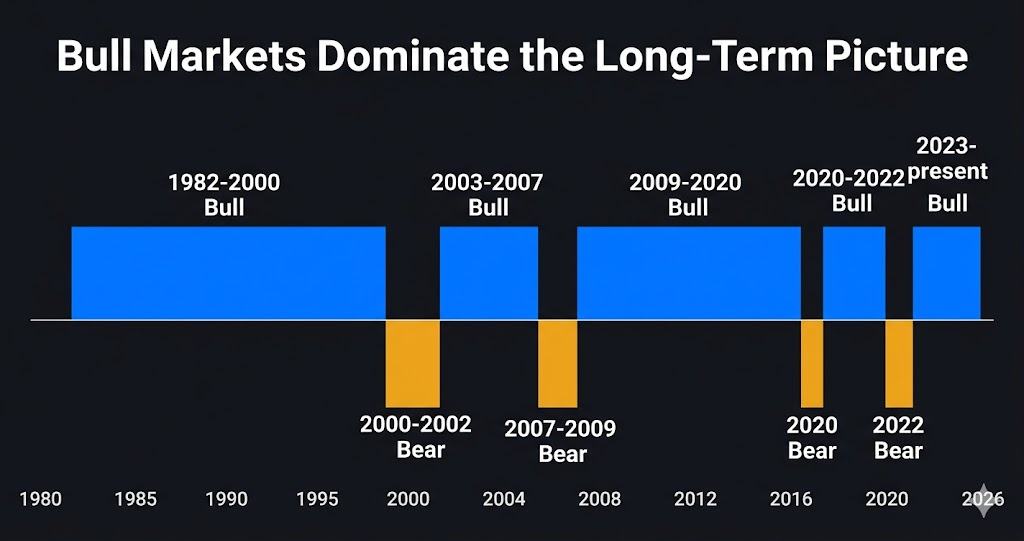

- The longest bull market on record ran from 2009 to 2020, lasting approximately 11 years and gaining over 400 percent.

- The shortest bear market on record was the 2020 pandemic crash, lasting approximately 33 days.

- The most severe bear market since World War II was 2007 to 2009, with the S&P 500 declining approximately 57 percent peak to trough.

- The dot-com bear market of 2000 to 2002 lasted approximately 30 months and declined roughly 49 percent.

- Every bear market in S&P 500 history has been followed by a bull market that exceeded the prior peak.

That last point deserves emphasis. Not some bear markets have been followed by recoveries. All of them have. That is not a guarantee about the future. It is a powerful statement about the historical resilience of diversified equity markets.

The Key Differences Between Bull and Bear Markets

Beyond the 20 percent threshold definition, bull and bear markets differ across several important dimensions that affect how investors should think and act.

- Duration. Bull markets average 6.6 years. Bear markets average 1.3 years. The asymmetry strongly favors staying invested.

- Magnitude. Average bull market gains of 339 percent dwarf average bear market losses of 38 percent. The math of compounding works in the long-term investor’s favor.

- Emotional intensity. Bear markets generate far more psychological pressure than bull markets despite being shorter and smaller in magnitude. Fear is a more powerful emotion than greed, which is why bear markets feel more significant than they statistically are.

- Media coverage. Bull markets generate optimistic coverage that accelerates in the late stage. Bear markets generate catastrophist coverage that peaks near the bottom. Both are lagging indicators, not leading ones.

- Opportunity. Bull markets reward those already invested. Bear markets create the entry points that generate the best long-term returns for investors with capital and conviction.

What to Do in a Bull Market

Bull markets are not a time to be passive. They are a time to be disciplined about what you own and what you are paying for it.

In the early and mid stages, stay fully invested and let compounding work. Resist the temptation to hold cash waiting for a pullback that may not arrive for years. Missing even a portion of a bull market’s gains is extremely difficult to make up.

In the late stage, reassess valuations. When the stocks you own are trading at multiples that require extraordinary future growth to justify, trimming positions and raising some cash is not market timing. It is portfolio hygiene. The goal is not to predict the top. It is to avoid being fully exposed at prices that leave no margin of safety.

For investors looking for research that identifies specific opportunities within a bull market’s later stages, Altucher’s Investment Network takes a contrarian, opportunistic approach to finding asymmetric ideas that the broader bull market has not yet fully priced in. It is a useful complement to a core index fund position when you want exposure to higher-conviction individual ideas.

What to Do in a Bear Market

Bear markets are not a time to panic. They are a time to execute the plan you built before the bear market started.

The first priority is assessing what you own. A bear market reveals which positions you hold because you have genuine conviction and which you hold because they went up. Positions in businesses with deteriorating fundamentals should be sold regardless of the loss. Positions in businesses with intact fundamentals and compressed valuations should be held or added to.

The second priority is managing cash. Investors who enter bear markets with some cash reserves have options that fully deployed investors do not. Deploying that cash into quality businesses at bear market prices is one of the most reliable wealth-building moves in investing. It requires the psychological ability to buy when everything feels wrong.

For macro-focused analysis that helps investors understand the structural forces driving bear markets and position defensively, Jim Rickards’ Strategic Intelligence focuses on geopolitical risk, gold, and the kinds of systemic vulnerabilities that tend to accelerate during market downturns. Rickards’ framework is specifically built for investors who want to understand bear market catalysts before they materialize.

The One Mistake That Destroys Bull and Bear Market Returns

The single most expensive mistake investors make across both bull and bear markets is the same one: letting short-term price movement override long-term business judgment.

In bull markets, this means chasing momentum into overvalued positions because prices are rising. In bear markets, it means selling quality businesses at distressed prices because the portfolio looks painful. Both errors are driven by the same underlying cause: treating price as a signal about business quality rather than market sentiment.

The antidote is a framework built before you need it. Know what you own. Know why you own it. Know at what price it becomes genuinely overvalued and at what price it becomes a genuine bargain. That framework, applied consistently across full market cycles, is what separates investors who build wealth from those who simply experience volatility.

For the broader context on how bull and bear markets fit into the larger pattern of market cycles, see our pillar guide to market cycles explained. For a deeper look at what triggers the most severe bear markets, see our guide to what causes stock market crashes.

Wall Street Reality Check

The financial industry profits from your activity, not your returns. Bull markets generate optimistic research reports and new product launches designed to capture money flowing into equities. Bear markets generate defensive products, hedging strategies, and fear-based marketing designed to capture money flowing out. Neither is designed with your long-term wealth as the primary objective. The investors who ignore most of what Wall Street produces during both phases and stick to a simple, evidence-based strategy consistently outperform those who respond to the industry’s cycle-driven marketing.

Bottom Line

Bull markets and bear markets are not opposites to be feared and chased. They are two phases of the same ongoing cycle, each with its own emotional character and its own set of opportunities. The investors who understand both phases before they arrive make better decisions in both. Build the framework now. The next bear market will test it. The one after that will reward it.

Further Reading

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice. StockHitter.com and Jenna Lofton are not registered investment advisors. All investing involves risk, including the potential loss of principal. Past performance does not guarantee future results. Always conduct your own due diligence and consult a licensed financial professional before making investment decisions. Jenna Lofton holds a position in PLTR. Some links on this page may be affiliate links, meaning StockHitter.com may receive compensation if you subscribe to a service at no additional cost to you. This does not influence our editorial opinions.