Value Investing: How to Find Stocks Below Their Worth

Updated: May 2026 | By Jenna Lofton, StockHitter.com

Jenna’s Bottom Line

Value investing is not about finding cheap stocks. It is about finding great businesses the market has temporarily mispriced. The difference between those two things determines whether you build wealth or collect a portfolio of value traps. Master that distinction and everything else in this guide becomes useful.

Key Takeaways

- Value investing means buying stocks trading below their intrinsic business value with a margin of safety that protects against being wrong.

- Benjamin Graham formalized the strategy. Warren Buffett refined it by adding business quality as a filter alongside price. Both elements matter.

- The four primary value metrics are price-to-earnings ratio, price-to-book ratio, free cash flow yield, and EV/EBITDA. No single metric tells the full story.

- Value traps are stocks that look cheap on metrics but are cheap for a reason. Declining competitive position, industry disruption, and deteriorating management are the most common causes.

- Value investing is not dead in the AI era. It has migrated toward AI-adjacent businesses that receive less media attention than the headline names but generate real and growing earnings.

What Value Investing Actually Is

Value investing is the practice of buying businesses at prices below their intrinsic value. Intrinsic value is what a business is actually worth based on its assets, earnings power, and future cash flow, independent of what the market currently says it is worth.

The core insight behind value investing is that markets are frequently wrong in the short term. Sentiment, momentum, and fear drive prices above and below fair value constantly. Patient investors who can identify those mispricings and wait for the gap to close generate above-average returns over time.

That sounds simple. The execution is anything but. Estimating intrinsic value accurately requires genuine understanding of financial statements, competitive dynamics, and industry economics. Getting it wrong in the direction of overestimating value is exactly how value investors end up holding value traps for years.

The Origins: Graham and Buffett

Benjamin Graham developed the intellectual framework for value investing in the 1930s and codified it in his books Security Analysis and The Intelligent Investor. Graham’s approach was quantitative and conservative. He focused on buying stocks at significant discounts to their net asset value with strict criteria around balance sheet strength and earnings consistency.

Warren Buffett studied under Graham at Columbia Business School and spent his early career applying Graham’s framework literally. His later evolution, influenced by Charlie Munger, added a critical dimension Graham underweighted. Business quality matters as much as price. A wonderful business at a fair price outperforms a fair business at a wonderful price over long time horizons.

The modern value investing framework combines both insights. Price discipline from Graham. Quality filtering from Buffett. Neither alone is sufficient.

The Margin of Safety Explained

The margin of safety is the central concept in value investing. It is the gap between a stock’s intrinsic value and the price you pay for it.

If you estimate a business is worth $100 per share and buy it at $65, your margin of safety is 35 percent. That gap serves two purposes. It protects you if your valuation estimate is wrong. And it amplifies returns when the market eventually reprices the business toward fair value.

Graham recommended buying only when the margin of safety was substantial, typically 33 percent or more. That conservatism filters out marginal opportunities and forces discipline around price. Buffett has operated with narrower margins of safety on businesses with exceptional competitive advantages, accepting less price cushion in exchange for higher quality.

Key Value Investing Metrics

No single metric defines value. The most effective value investors use multiple lenses simultaneously to build a complete picture of whether a business is genuinely underpriced.

The four metrics that matter most:

- Price-to-Earnings Ratio (P/E). The most widely used valuation metric. It measures how much investors pay for each dollar of annual earnings. A P/E of 15 means you are paying $15 for every $1 of profit. Context matters enormously. A P/E of 15 is expensive for a declining business and cheap for one growing earnings at 20 percent annually.

- Price-to-Book Ratio (P/B). Compares the stock price to the accounting book value of the company’s assets. Graham focused heavily on this metric. A P/B below 1.0 theoretically means you are buying a dollar of assets for less than a dollar. In practice, book value understates the worth of intangible assets like brand, software, and customer relationships, which limits this metric’s usefulness for modern businesses.

- Free Cash Flow Yield. Free cash flow is the actual cash a business generates after capital expenditures. Dividing free cash flow by market cap gives you the free cash flow yield, which is arguably the most honest measure of what a business actually earns versus what accounting rules say it earns. A free cash flow yield above 6 to 7 percent in the current rate environment typically signals genuine value.

- EV/EBITDA. Enterprise value divided by earnings before interest, taxes, depreciation, and amortization. This metric accounts for a company’s debt load, which P/E ignores. It is particularly useful for comparing businesses with different capital structures or for evaluating companies with significant depreciation that distorts reported earnings.

For a deeper breakdown of how these metrics work in practice, see our dedicated guides to P/E ratio and EV/EBITDA.

How to Identify Value Traps

A value trap is a stock that appears cheap on metrics but is cheap for a fundamental reason that the metrics do not capture. Buying value traps is the most common and most expensive mistake in value investing.

The most reliable warning signs of a value trap:

- Declining competitive position. A business losing market share to better competitors will see earnings erode regardless of how cheap it looks today. The low P/E reflects the market pricing in future earnings decline, not a mispricing.

- Industry disruption. Businesses in industries being structurally disrupted by technology, regulation, or changing consumer behavior can look cheap for years while their intrinsic value steadily declines. Traditional retail, print media, and legacy telecommunications are examples from the past two decades.

- Deteriorating balance sheet. Rising debt, declining cash, and shrinking margins are warning signs that a cheap stock may get cheaper. Graham’s emphasis on balance sheet strength was specifically designed to filter out these situations.

- Management capital allocation failures. Companies that consistently make poor acquisitions, overpay for buybacks at peak prices, or accumulate cash without a clear deployment plan are destroying shareholder value regardless of their reported earnings.

The test that separates genuine value from a value trap is simple in theory and hard in practice. Ask why the stock is cheap. If the answer is temporary pessimism about a business with durable earnings power, that is value. If the answer is that the business model is structurally challenged, that is a trap.

Experience Transparency

My most expensive value investing mistakes have almost all been value traps. A regional bank trading at 0.6 times book value that looked like Graham’s ideal candidate. It turned out the loan book had credit quality issues that the balance sheet did not reflect yet. A media company at 8 times earnings that looked cheap until cord-cutting accelerated and the earnings base collapsed. Both situations passed the basic metric screens. Neither passed the honest question of why the stock was cheap. I learned to spend as much time on that question as on the valuation work itself. Metrics get you to the table. Business analysis determines whether you should sit down.

Value Investing vs Growth Investing

Value and growth investing are often framed as opposites. In practice the best investors treat them as a spectrum rather than a binary choice.

Pure value investing, buying statistically cheap stocks without regard for growth, has underperformed in the post-2010 environment dominated by technology and AI infrastructure. The businesses that looked cheap on traditional metrics often deserved to be cheap. The businesses that looked expensive on traditional metrics often deserved their premium because their earnings growth justified it.

The more useful framework is growth at a reasonable price (GARP), which combines value discipline around not overpaying with growth awareness that some businesses deserve premium multiples. Buffett’s annual letters to Berkshire Hathaway shareholders describe this evolution explicitly, moving from Graham’s pure statistical cheapness toward paying fair prices for exceptional businesses.

For our full breakdown of growth investing and when paying a premium makes sense, see our guide to growth investing.

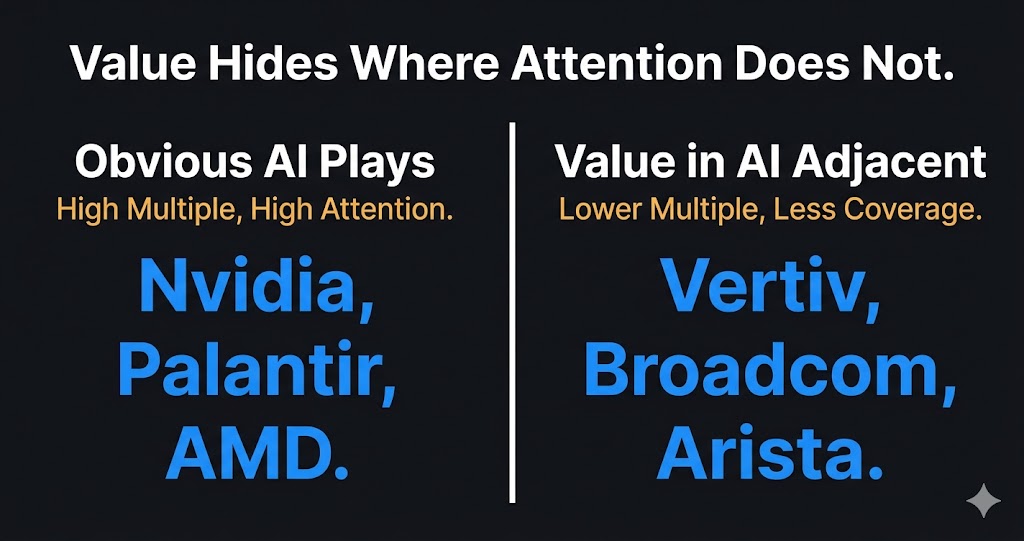

Value Investing in the AI Era

Value investing is not dead in the current AI-dominated market. It has migrated toward businesses that benefit from the AI infrastructure build-out but receive far less media attention than the headline names.

The obvious AI plays, companies like Nvidia and Palantir Technologies (PLTR), trade at multiples that traditional value investors cannot justify. That is not a mispricing. It reflects genuine earnings power growth that the market is pricing correctly.

The value opportunity in the AI cycle lies in adjacent businesses. Companies supplying power infrastructure, cooling systems, networking hardware, and data center construction materials are generating real and growing earnings from AI capital expenditure while trading at multiples far below the software platforms getting the most attention. Vertiv and Arista Networks (ANET) are examples of businesses where genuine value analysis reveals earnings power that the market has been slower to price in than the obvious AI plays.

For our full analysis of the AI infrastructure theme and where value opportunities currently exist within it, see our guide to best AI infrastructure stocks to watch in 2026.

How to Apply Value Investing: A Practical Process

Value investing without a repeatable process is just opinion dressed up as analysis. Here is the process that works:

- Screen for candidates. Use a stock screener to filter for businesses trading at low P/E, low P/B, or high free cash flow yield relative to their sector peers. Finviz’s stock screener allows multi-factor filtering at no cost and is the starting point most professional value investors use for initial candidate generation.

- Understand the business. Before any valuation work, confirm you understand what the business does, how it makes money, who its competitors are, and what its competitive advantage is. If you cannot explain this clearly, stop here.

- Estimate intrinsic value. Use discounted cash flow analysis, comparable company multiples, or asset-based valuation depending on the business type. Run multiple scenarios. Your base case, a bear case, and a bull case. The range of outcomes tells you as much as the point estimate.

- Calculate the margin of safety. Compare your intrinsic value estimate to the current market price. Only proceed if the margin of safety is meaningful, typically 25 percent or more.

- Ask why it is cheap. This is the most important step. A business with a real margin of safety that you cannot explain the cheapness of is either a genuine opportunity or a value trap you have not identified yet. Keep digging until you have a satisfying answer.

- Set a price target and a sell discipline. Know in advance at what price you will consider the position fully valued and begin reducing. Value investing without a sell discipline produces investors who hold forever and confuse patience with stubbornness.

For investors who want institutional-grade analytical support applied to this kind of value-focused fundamental research, Hidden Alpha from Joel Litman uses Uniform Accounting methodology to restate financial statements in ways that remove the distortions standard accounting creates. It frequently identifies significant gaps between reported earnings and real earnings power that traditional value screens miss entirely.

Wall Street Reality Check

Value investing has been declared dead approximately once per decade since Graham first wrote about it in the 1930s. It was dead during the Nifty Fifty era of the 1960s. Dead again during the dot-com boom. Dead again during the 2010s technology bull market. Each declaration came near the peak of a growth cycle when momentum strategies were producing the best returns and patience looked like a character flaw. Value has consistently recovered its relevance in the periods that followed. The strategy is not dead. It requires more analytical rigor in an era of intangible-asset-heavy businesses than it did when Graham was buying companies at discounts to their physical assets. That is a higher bar, not an obituary.

Bottom Line

Value investing works when applied with genuine analytical rigor and the patience to hold through the periods when the market disagrees with your assessment. It requires understanding businesses deeply enough to estimate what they are actually worth, the discipline to buy only when the price offers a real margin of safety, and the judgment to distinguish genuine mispricings from value traps. That combination is rare. It is also one of the most reliably profitable approaches in investing history when executed properly.

Further Reading

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice. StockHitter.com and Jenna Lofton are not registered investment advisors. All investing involves risk, including the potential loss of principal. Past performance does not guarantee future results. Always conduct your own due diligence and consult a licensed financial professional before making investment decisions. Jenna Lofton holds a position in PLTR. Some links on this page may be affiliate links, meaning StockHitter.com may receive compensation if you subscribe to a service at no additional cost to you. This does not influence our editorial opinions.